For most low-income families around the world, owning a home represents much more than a financial decision.

It represents dignity. Stability. Safety. The feeling of finally standing on solid ground.

The idea of home ownership is often sold as the ultimate symbol of success:

“Once you have your own place, everything else becomes easier.”

But for millions of people, that promise slowly turns into anxiety, pressure, and long-term financial stress.

This article is not here to destroy the dream of owning a home.

It is here to ask an honest question that few people dare to ask before signing a financing contract:

Is home ownership really financial freedom for low-income families — or can it quietly become a lifelong trap?

Why owning a home feels like the safest investment

For someone with limited income, traditional investments often feel inaccessible.

Stocks feel risky.

Businesses feel uncertain.

Savings feel slow.

A house, on the other hand, feels tangible.

You can touch it.

You can live in it.

You can see it every day.

That physical presence creates a powerful sense of security. For many families, it feels like the first real asset they will ever own.

And culturally, this belief is reinforced everywhere:

- “Rent is money thrown away.”

- “At least with a house, you’re paying something that will be yours.”

- “Property always goes up in value.”

These ideas are repeated so often that they start to feel like facts.

But they are incomplete truths.

Is home ownership really financial freedom for low-income families

When a home is an asset — and when it is a liability

A home can be an asset.

But it is not automatically one.

The difference lies in timing, income stability, and debt structure.

For a high-income household with strong savings and financial buffers, a mortgage may represent a manageable commitment.

For a low-income family, the same mortgage can become a fragile balancing act where one unexpected event is enough to break everything.

A home becomes a liability when:

- the monthly payment consumes too much income

- the budget has no flexibility

- savings are sacrificed to “just keep the house”

- fear replaces peace

At that point, the house is no longer providing security — it is demanding it.

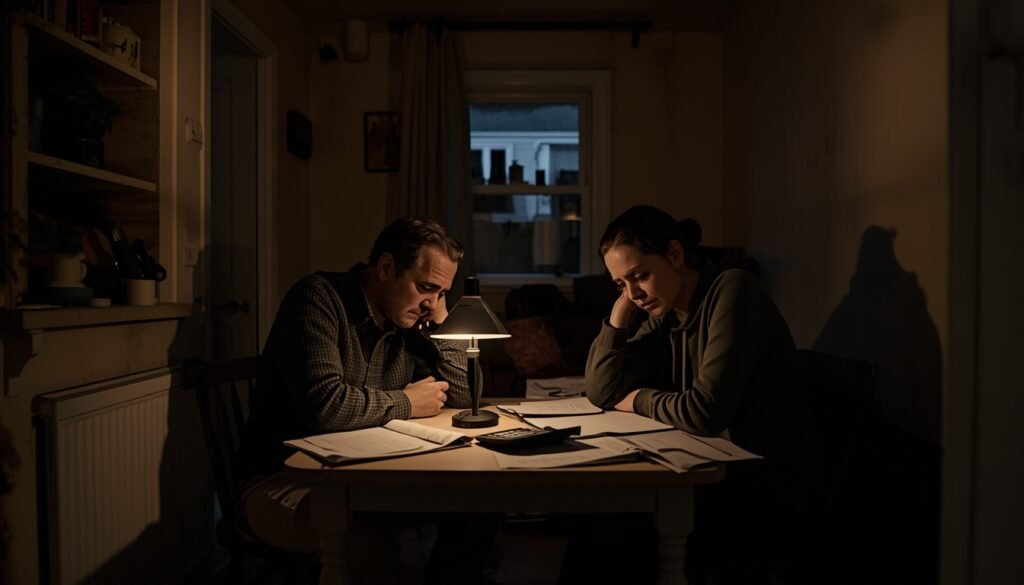

The emotional pressure behind the decision

One of the most dangerous forces in home financing is not interest or contracts.

It is emotional pressure.

Low-income families often feel:

- fear of missing their only chance

- pressure from family and society

- shame for still renting

- urgency created by rising prices

This pressure pushes people to buy before they are ready, not because the numbers make sense, but because emotionally it feels like “now or never.”

And once the decision is made, there is rarely space to turn back.

The hidden risks of home financing no one explains to low-income buyers

Here is where most advice fails.

Banks explain interest rates.

Real estate agents explain properties.

But very few people explain risk from the buyer’s perspective.

Risk #1: Income fragility

Low-income households usually depend on:

- one main income

- unstable work

- limited job security

A mortgage assumes consistency over decades.

That mismatch alone creates vulnerability.

Risk #2: The percentage of income trap

This is one of the most important parts of this entire discussion.

A safe mortgage payment for low-income families generally follows this logic:

- Up to 25% of net monthly income → manageable zone

- Around 30% → risk zone

- Above 35% → danger zone

And this calculation should include:

- mortgage payment

- mandatory insurance

- taxes

- maintenance

- variable interest adjustments

What looks like 30% on paper often becomes 40% in real life.

At that point, the house starts controlling the family — not the other way around.

Risk #3: No margin for life

Life is not stable for 30 years.

People get sick.

Jobs change.

Families grow.

Expenses rise.

When a mortgage leaves no margin, every small problem becomes a financial emergency.

This constant pressure slowly destroys the sense of “freedom” the house was supposed to provide.

Why financing feels affordable at first

Banks are experts at making numbers look comfortable today.

Long terms.

Small installments.

Optimistic projections.

What is rarely emphasized is how much interest accumulates over time and how little flexibility exists once the contract is signed.

For low-income families, this structure is especially dangerous because:

- refinancing options are limited

- emergency savings are usually small

- selling the property is not always easy or quick

The myth of “at least it will be mine one day”

This phrase hides a painful truth.

Ownership at the end of 30 years does not erase:

- decades of stress

- lost opportunities

- financial sacrifices

- postponed life decisions

Freedom is not about future ownership alone.

It is about present stability.

When renting is not failure

Renting is often framed as a mistake.

In reality, renting can be:

- a form of flexibility

- a protection against debt

- a strategic choice during unstable income phases

For some families, renting while building financial resilience is far safer than locking into a mortgage that leaves no room to breathe.

The question few people ask before buying

Instead of asking:

“Can I get approved?”

A better question is:

“If my income drops for six months, will I still be okay?”

If the answer is no, the problem is not the house — it’s the timing.

What real financial freedom actually looks like

For low-income families, financial freedom is not about ownership at any cost.

It is about:

- predictability

- flexibility

- safety

- peace of mind

A home that creates fear is not freedom.

If the first part of this article planted doubt, this second part is about clarity.

Not to scare.

Not to discourage.

But to help families avoid decisions that silently lock them into decades of stress.

How long-term financing changes your life without you noticing

Mortgages are long.

Very long.

Twenty. Thirty. Sometimes forty years.

At the beginning, that length feels comforting. Smaller payments feel manageable.

But time is not neutral.

Over decades:

- interests accumulate

- life circumstances change

- priorities shift

- energy decreases

What felt acceptable at 30 may feel suffocating at 50.

Interest: the invisible cost no one feels at first

Interest doesn’t hurt immediately.

It hurts slowly.

Most buyers focus on the monthly payment, not the total amount paid over time.

For low-income families, this is critical.

Paying two or three times the property’s value over decades means:

- less money for emergencies

- less money for education

- less money for health

- less ability to adapt

Insurance, taxes, and maintenance: the forgotten costs

Owning a home is not just the mortgage.

It also includes:

- mandatory insurance

- property taxes

- repairs

- unexpected maintenance

These costs don’t disappear during hard times.

They arrive no matter what.

What happens when income drops

This is where many families get trapped.

When income falls:

- the house cannot be “paused”

- the bank doesn’t wait

- stress increases rapidly

Selling a financed home is not always simple, especially in bad markets.

What was supposed to be stability becomes a source of constant fear.

Why foreclosure is not the only loss

Even without foreclosure, families lose:

- mental health

- sleep

- freedom of choice

- mobility

- long-term growth

A house can silently drain life quality while still being “owned.”

The generational impact

One of the most painful consequences of bad home financing decisions is generational.

Parents sacrifice everything to keep the house.

Children grow up inside financial stress.

Opportunities are limited.

The house survives — but the family’s flexibility doesn’t.

When buying a home does make sense

This article is not anti–home ownership.

Buying a home can make sense when:

- income is stable

- the payment stays below safe percentages

- emergency savings exist

- the decision is calm, not rushed

Timing matters more than desire.

A healthier way to think about home ownership

Instead of asking:

“Is owning a home success?”

Ask:

“Does this home increase or reduce my financial resilience?”

That answer is different for every family — and that’s okay.

Continue learning with clarity

If this article made you think, these related guides may help you explore finances with more confidence and less pressure:

- Should you pay off debt before investing?

- Why financial stress keeps families stuck

- How long-term debt quietly reshapes life decisions

- Why stability matters more than ownership

Final reflection

For low-income families, a home can be:

- a foundation

- or a cage

The difference is not the dream.

It is the structure behind it.

Understanding risks does not kill dreams.

It protects them.