Saving money and financial stability are two goals that millions of people talk about but very few feel they truly understand.

Many people work hard, receive a steady paycheck, and still feel like their financial situation never really improves. Bills keep coming, expenses appear unexpectedly, and the idea of long-term stability seems distant.

If you’ve ever asked yourself questions like these, you are not alone:

- Why does saving money feel so difficult?

- Why do some people build financial stability while others struggle for years?

- Is it still possible to improve your financial situation even if you feel behind?

The truth is that financial stability rarely happens by accident.

For most households, it develops through a combination of simple habits, awareness, and consistent financial decisions made over time.

This guide will explain how saving money and building financial stability really work in real life. Instead of complicated financial theories, we will focus on practical ideas that ordinary people can understand and apply.

By the end of this article, you will understand:

- why saving money feels difficult for many people

- the key steps that create financial stability

- how budgeting and emergency savings protect your finances

- small financial habits that can improve your situation over time

Financial stability is not about perfection.

It is about creating a system that helps you make better financial decisions consistently.

Why Saving Money Feels Difficult for Many People

One of the most common frustrations people experience is the feeling that saving money should be simple, yet in reality it feels extremely difficult.

The reason is that financial pressure usually comes from several factors happening at the same time.

Rising housing costs, healthcare expenses, transportation, and daily living costs often consume a large portion of household income. Even when salaries increase, expenses often grow as well.

This creates a cycle where people feel like they are working harder but not necessarily getting ahead financially.

Another factor is the lack of clear financial structure.

Many households never develop a clear system for managing their income. Money enters the account, bills are paid, everyday expenses accumulate, and whatever remains at the end of the month determines whether saving is possible.

Without a plan, saving money becomes unpredictable.

This pattern is closely related to the financial behaviors discussed in Why You’re Always Broke (Even When You Make Decent Money), where everyday financial habits slowly shape long-term financial outcomes.

Understanding these patterns is the first step toward improving financial stability.

The First Step to Financial Stability: Understanding Your Money

Financial stability begins with awareness.

Before anyone can improve their financial situation, they need to understand exactly how money flows through their life.

Many people are surprised when they begin tracking their spending for the first time. Small everyday expenses that once felt insignificant suddenly add up to meaningful amounts.

Examples include:

- food delivery and convenience spending

- recurring subscriptions

- small impulse purchases

- service fees and automatic payments

Individually these expenses seem harmless, but together they can quietly affect a household’s ability to save money.

Developing daily awareness about money is one of the most powerful financial habits a person can build.

Several small habits that help improve financial awareness are explored in Daily Money Habits That Quietly Improve Your Financial Life (2026).

Financial stability begins not with complex strategies, but with understanding the basic relationship between income, spending, and saving.

The Role of Budgeting in Building Financial Stability

Budgeting often has a negative reputation.

Many people associate budgeting with strict limitations or the idea of constantly restricting their lifestyle.

In reality, budgeting simply provides structure.

A good budget does not exist to control every detail of your spending. Instead, it helps ensure that your money is being used intentionally rather than disappearing unexpectedly.

A basic budget usually includes three essential categories:

- essential living expenses

- financial protection (savings)

- flexible spending

When a person understands how much money belongs in each category, financial decisions become much easier.

A simple and practical approach to budgeting is explained in Simple Budget That Works: How to Create One That Actually Lasts (2026).

Budgeting does not need to be complicated to be effective. Even a simple structure can significantly improve financial stability over time.

The Hidden Expenses That Quietly Destroy Financial Progress

One of the biggest reasons people struggle to build savings is not always large expenses, but rather hidden everyday spending.

These expenses rarely attract attention because they happen gradually and often automatically.

Examples include:

- unused subscriptions

- convenience purchases

- recurring service fees

- small impulse spending

Individually these purchases feel small, but over months and years they can quietly drain thousands of dollars from a household budget.

Learning to recognize these financial leaks can dramatically improve a person’s ability to save money.

Many of these spending patterns are discussed in detail in Hidden Expenses That Quietly Drain Your Money.

Identifying these hidden expenses often becomes one of the easiest ways to begin improving financial stability.

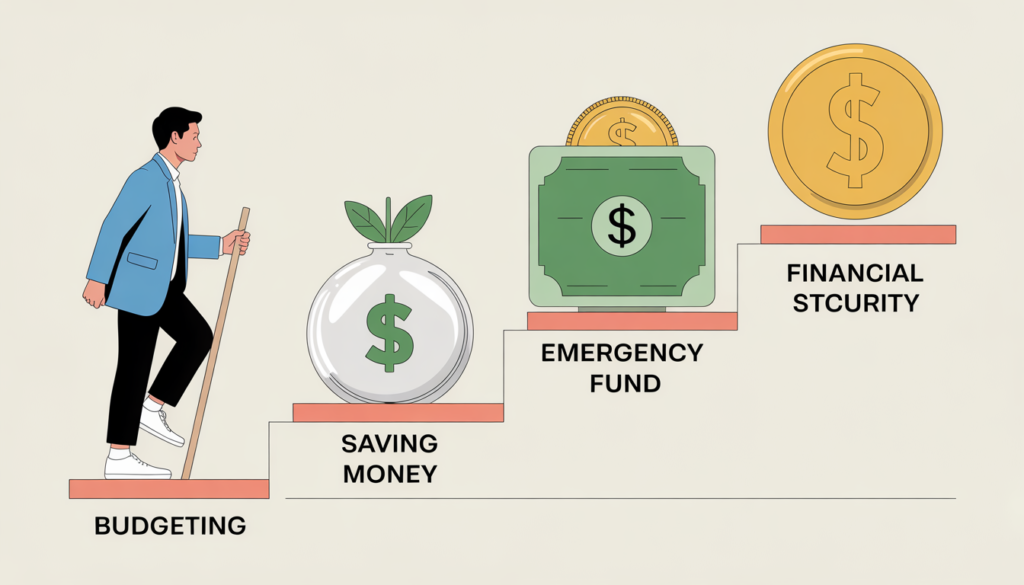

The Four Foundations of Financial Stability

While financial situations vary widely, most financially stable households follow a similar structure.

Financial stability usually develops through four key foundations.

| Financial Step | Why It Matters | Example Action |

|---|---|---|

| Financial Awareness | Understand where money goes | Track spending habits |

| Budget Control | Manage income and expenses | Create a simple monthly budget |

| Emergency Protection | Prevent financial crises | Build an emergency fund |

| Consistent Saving | Strengthen long-term security | Save money regularly |

These four foundations do not require advanced financial knowledge.

They simply require consistent attention to how money is managed.

Over time, these habits create a stable financial environment that protects households from unexpected financial stress.

Why Emergency Funds Are One of the Most Important Financial Tools

One of the biggest differences between financially stable households and financially vulnerable households is the presence of an emergency fund.

Unexpected expenses are a normal part of life.

Cars break down. Medical bills appear. Appliances stop working. Temporary job interruptions occur.

Without emergency savings, these events often lead to debt.

With emergency savings, they become manageable inconveniences instead of financial disasters.

An emergency fund acts as a financial safety cushion.

For readers interested in building this safety net, a practical step-by-step explanation is available in How to Build an Emergency Fund From Zero (Even If You Live Paycheck to Paycheck).

Even a modest emergency fund can dramatically reduce financial stress.

How Saving Money Builds Long-Term Financial Stability

Saving money consistently creates financial flexibility.

When households develop the habit of saving regularly, they gain options. Unexpected expenses become manageable. Financial goals become achievable. Long-term planning becomes possible.

Savings provide more than financial security.

They provide peace of mind.

Instead of reacting to every financial challenge, people with savings can respond with greater confidence and stability.

Even small savings contributions, when practiced consistently, can accumulate into meaningful financial protection over time.

Financial stability is rarely the result of one large financial decision.

It is usually the result of many small decisions made consistently over many years.

How Much Should You Save Over Time?

One of the most common questions people ask when thinking about saving money and financial stability is simple:

How much money should I actually have saved by a certain age?

This question matters because it helps people understand whether their current financial habits are helping them move forward or holding them back.

Financial experts often use general benchmarks to illustrate how savings can grow over time. These benchmarks are not strict rules, but they can provide a useful reference point for evaluating long-term financial progress.

Below is a simplified comparison used by many financial planners.

Savings Benchmarks by Age

| Age | Suggested Savings | Financial Goal |

|---|---|---|

| 30 | Around 1× yearly salary | Build the habit of saving |

| 40 | Around 3× yearly salary | Strengthen financial stability |

| 50 | Around 6× yearly salary | Prepare for long-term financial security |

For example, if someone earns $60,000 per year:

- By age 30 → about $60,000 saved

- By age 40 → about $180,000 saved

- By age 50 → about $360,000 saved

These numbers are not meant to create pressure. Instead, they help illustrate the general pace that long-term savings often require.

Life circumstances vary widely, and many people face financial challenges that affect their ability to save consistently.

However, understanding these benchmarks helps people identify whether adjustments might improve their financial trajectory.

Readers who want to explore this topic in greater detail can learn more in How Much Money Should You Have Saved by Age 50?.

What If You Feel Behind Financially?

Many readers reach this part of the discussion and feel discouraged.

They compare their current savings with financial benchmarks and realize they are not where they expected to be.

This situation is extremely common.

In fact, surveys consistently show that many households approach retirement age with limited savings.

But feeling behind financially does not mean improvement is impossible.

Financial progress does not require perfection.

It requires momentum.

Small improvements in financial habits can still create meaningful progress over time.

Some examples include:

- reducing unnecessary expenses

- increasing monthly savings gradually

- paying down high-interest debt

- strengthening financial awareness

Even modest improvements can significantly improve financial stability in the long term.

Where Should You Keep Your Savings?

Another common question people ask when thinking about saving money and financial stability is where those savings should be stored.

For most households, the most important factors are:

- safety

- accessibility

- simplicity

The goal is not to chase risky investment opportunities. Instead, the focus should be on protecting financial stability.

Here are several common options many Americans use.

Savings Accounts

Savings accounts remain one of the most common ways people store their money.

While the interest rates are typically modest, savings accounts offer several advantages:

- funds remain easily accessible

- deposits are generally protected by financial regulations

- money is separated from everyday spending accounts

For emergency funds, savings accounts are often one of the safest and simplest solutions.

Retirement Accounts

Many Americans also use retirement accounts to build long-term savings.

These accounts are designed to help people gradually accumulate funds that will support them later in life.

Because retirement accounts are typically intended for long-term use, they are usually separate from everyday savings.

That is why many financial planners recommend building both:

- an emergency fund for unexpected expenses

- retirement savings for long-term financial security

Conservative Investment Options

Some households choose to place part of their savings into relatively conservative investment options that aim to balance safety and modest growth.

The most important principle is avoiding overly complex financial strategies that may introduce unnecessary risk.

Financial stability often benefits more from consistency and discipline than from chasing aggressive investment returns.

Small Financial Habits That Build Stability

When people imagine improving their finances, they often assume that dramatic changes are required.

In reality, long-term financial stability is usually built through small habits practiced consistently.

Here are several habits that gradually strengthen financial security.

Reviewing Your Finances Regularly

Checking financial accounts regularly helps people stay aware of their spending and saving patterns.

Even reviewing finances once per week can increase awareness and reduce impulsive spending.

Avoiding Lifestyle Inflation

Lifestyle inflation occurs when spending increases every time income increases.

While improving one’s quality of life is natural, constantly expanding expenses can prevent long-term savings from growing.

Redirecting a portion of income increases toward savings can significantly improve financial stability over time.

Reducing High-Interest Debt

Debt with high interest rates can significantly slow financial progress.

Credit card balances, in particular, can quietly accumulate interest that consumes a large portion of monthly income.

Understanding the behavioral patterns behind long-term debt is discussed further in The Real Reasons People Stay in Debt for Years.

Reducing high-interest debt often frees up money that can later strengthen savings.

Financial Habits That Strengthen Stability Over Time

The table below illustrates how simple financial behaviors can influence long-term financial outcomes.

| Financial Habit | Long-Term Benefit |

|---|---|

| Tracking expenses | Greater financial awareness |

| Creating a budget | Better control of spending |

| Building an emergency fund | Protection against unexpected expenses |

| Saving consistently | Gradual growth of financial security |

| Reducing high-interest debt | Less financial pressure |

These habits may appear simple, but over time they shape the financial stability of a household.

Financial progress rarely depends on one major decision. Instead, it results from consistent habits practiced for many years.

A Helpful Resource for Financial Planning

Readers who want additional guidance on budgeting and saving can explore resources from the Consumer Financial Protection Bureau, a U.S. government agency focused on financial education and consumer protection.

Their website offers practical tools designed to help households understand spending, manage debt, and improve financial planning.

You can explore their budgeting resources here:

External resources like this provide helpful information for people who want to strengthen their financial knowledge and make more informed financial decisions.

The Real Meaning of Financial Stability

Many people imagine financial stability as a perfect situation where money problems never exist.

In reality, financial stability means something different.

It means having enough structure in your financial life to handle challenges without constant stress.

Financial stability usually includes:

- understanding your income and expenses

- maintaining an emergency fund

- avoiding excessive debt

- saving money consistently

When these elements are present, households are better prepared for both expected and unexpected financial events.

Final Thoughts

Saving money and building financial stability is a long-term process.

There is rarely a single moment when financial stability suddenly appears.

Instead, it develops gradually through everyday financial decisions.

Understanding how money flows through your life, controlling spending habits, building emergency protection, and saving consistently all contribute to stronger financial security.

Even small improvements can create meaningful progress over time.

Financial stability is not reserved for people with perfect financial situations.

It is built by people who develop consistent financial habits and gradually improve their financial decisions year after year.

FAQ

Why is saving money so difficult for many people?

Saving money often feels difficult because everyday expenses consume a large portion of income. Without a clear financial structure, it becomes difficult to consistently set money aside.

How can I start saving money if my income is limited?

Starting small is often the most effective approach. Even modest savings contributions can grow over time when practiced consistently.

What is the first step toward financial stability?

The first step is understanding how money flows through your life. Tracking spending and creating a basic financial plan can significantly improve financial awareness.

How much money should I save each month?

Many financial planners recommend saving a portion of income regularly, but the exact amount varies depending on personal financial circumstances.

Readers interested in this topic can explore How Much Should You Save Each Month? A Simple Rule for Beginners (2026) (internal link).